How to avoid the child benefit tax charge

- By

- Murray Humphrey

With the cost of living crisis not showing any signs of slowing, it is more important than ever for parents to make the most of all their entitled benefits. Child benefit is a government-run scheme to help all parents with the costs of raising a child. However, since the introduction of the High Income Child Benefit Charge (HICBC) in January 2013, those earning in excess of £50,000 are liable for a tax charge, resulting in a loss of a portion of their child benefit.

In this article, we'll explore what that means and how you can avoid the child benefit tax charge altogether.

What is child benefit?

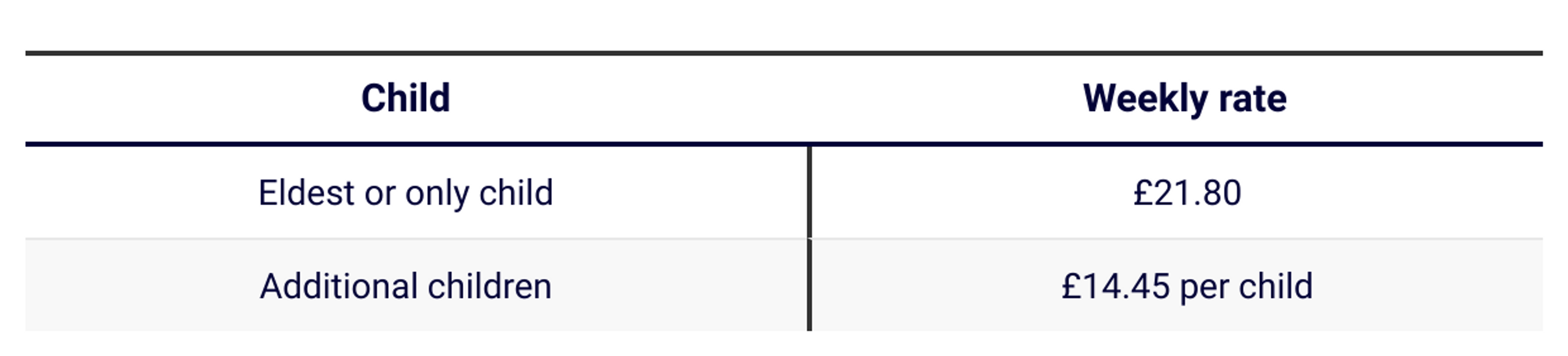

UK law states that, as a parent, you are entitled to child benefit for each child under the age of 16 (or up to the age of 20 years old if they are in formal education or an approved training program). The benefit is paid every 4 weeks with no limit on the number of children you can claim for. Only one parent can claim the child benefit for a given child. How much you get depends on

- how many children you have

- which child you are claiming for

Here's a quick example of what this means in the real world: A parent with an annual income of £35,000 with 2 children would be entitled to approximately £1,827.80 with no tax charge - around £152 each month.

What is the child benefit tax charge?

Any parent (or partner) with a yearly income over £50,000 is liable to pay a High Income Child Benefit Tax Charge.

Every £100 of income above the £50,000 threshold will see 1% of your total child benefit amount wiped out. This is calculated on the adjusted net income (ANI). For those with an income above £60,000, the tax charge will equal the same amount of the child benefit - effectively cancelling it out entirely.

This has been controversial - with some referring to it as the child benefit tax trap. The person liable for the tax charge is the parent with the higher income. For example, for a couple both earning in excess of £50,000, whoever has the highest income would be responsible for paying the charge at the end of the tax year.

However, for those affected by this tax trap, there is a solution - with some able to avoid this tax charge completely.

How to avoid the child benefit tax charge

One of the most straightforward ways to avoid the child benefit tax charge is simply to tell HMRC that you don't want to receive any child benefit. Naturally, this means you'll no longer be liable for any charges.

However, just because you don't wish to receive any child benefit, doesn't mean you shouldn't claim it. Let us explain. For non-working parents, it can still be beneficial to fill out a Child Benefit claim form as you it lets you earn National Insurance credits. This will impact the amount of State Pension you receive - as you need 35 years of National Insurance contributions to be eligible for the full new State pension. You'll need at least 10 years on your National Insurance record to qualify for any State pension.

Claiming Child Benefit then comes with fringe benefits too - so what are the best ways of avoiding the child benefit tax charge? Let's take a look.

1. Pension contributions

First up, your pension. Paying into your pension is one of the most tax-efficient and effective ways to reduce your annual net income (ANI). Pension contributions helps to reduce your taxable income, meaning you're less exposed to that £50,000-£60,000 child benefit tax charge bracket. Here's how it works.

The figure below shows the overall value of Child Benefit received for a couple with two children. In this example, one partner is working full time and earning £56,000 a year.

On the left, we can see the overall value of the child benefit received if the couple didn't make any pension contributions. As you can see, because their taxable income is £6,000 above the £50,000 threshold, the benefit is subject to a 60% tax charge. They have to pay back £1,131.

On the right, the same couple makes a pension contribution of £4,800 in the tax year. After receiving 20% tax relief, the total amount deductible from their income is £6,000.

This would then bring their overall taxable income down to £50,000. As a result, there would be no tax charge payable and the value of the child benefit would remain at £1,885. They've made a huge saving of £1,131 for the tax year - plus, as a higher earner, they could claim higher rate tax relief back via a self-assessment tax return.

2. Salary sacrifice

Another option for reducing your child benefit tax charge is through salary sacrifice. Here, you'll reduce your salary ' on paper' in exchange for another non-cash benefit. Popular examples include a pension contribution or childcare vouchers. To find out more about how salary sacrifice can trim your tax bill, check out our guide to salary sacrifice here.

3. Charitable donations & Gift Aid

You can also reduce your taxable income by making charitable donations under Gift Aid. Here, you won't save any tax yourself but will enable your charity of choice to get an extra 25% on top of your donation back from HMRC. This also helps cut your Child Benefit charge. All you'll need to do is add your Gift Aid donations to your tax return.

Conclusion

As we have seen, there are a few ways of avoiding the Child Benefit tax charge - with one of the most effective via paying into a pension. For those earning above the £50,000 threshold, there are huge savings to be made by regularly paying into a pension plan and reducing your annual net income figure back down toward £50,000.

Penfold is the award-winning, digital pension that helps you save more for the future. With a user-friendly app, you can finally combine all your pension into one, easy-to-manage place. Combine your old pensions in just a few taps today.

Murray Humphrey

Penfold