3 minutes

Deciphering the Hidden Costs of Workplace Pensions

- By

- Murray Humphrey

We’ve outlined some common extra charges from pension providers to assist accountants and advisers in making informed decisions for their clients.

At Penfold, we value transparency and hate extra charges, especially when it comes to financial management. We understand the fiduciary duty accountants have towards their clients, which is why we've crafted a fair, straightforward fee structure.

Our annual management fee on savers' pots covers everything, offering a cost-efficient solution for your clients. There are no fixed fees, extra fund management fees, account fees, or adviser fees for employers whatsoever. Similarly, we don’t charge employees extra admin charges, contribution charges, or to switch funds.

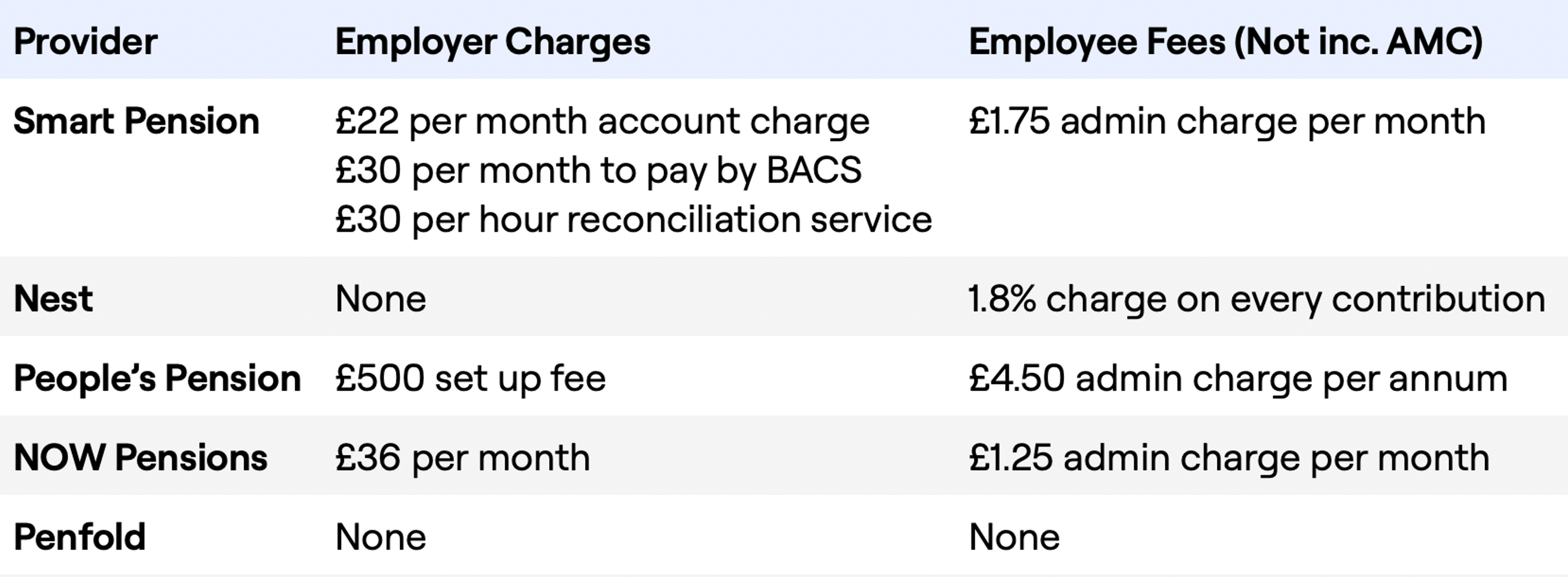

Most pension providers charge an annual management charge (AMC), but some also add extra charges on top, making it challenging to work out how much you will be paying. We’ve identified these in the table below:

Discover the potential savings awaiting your clients by switching to a transparent pension provider like Penfold. Our straightforward fee structure eliminates hidden charges, making financial planning easier and more predictable.

Get a glimpse of how Penfold can transform the pension management experience for you and your clients. The path to clearer, cost-effective pension solutions is just a click away.

Recent Charge Increases

Did you know that Smart Pension added a £15 per month employer charge on 1st December 2021?

They explained that they were introducing the charge "to improve the service we offer” and that it would “allow us to invest in our platform so that we can improve our service, as well as introduce new features and products to make your and your clients' lives easier."

The employer charge has recently risen to £22 per month.

The Impact of Extra Charges

There are 5.5m businesses classed as SMEs (small to medium sized enterprises) in the UK – 99% of all businesses according to the British government.1 The vast majority of them have less than 50 employees.

Since auto-enrolment was introduced in 2012, it’s mandatory for all of those small businesses to provide a workplace pension to their employees and contribute a minimum of 3% of their salaries into it. This usually makes it their most expensive workplace benefit.

The employer charges (such as the £36 monthly charge from NOW2) levied by some pension providers are an extra expense, but it’s a cost that can be avoided simply by switching providers, which the better pension companies out there make simple. Read how to change workplace pension provider.

Extra charges also have an impact on employees of course. Pension provider Nest charges individuals to put money into their pension, for example. If an employee is contributing £200 a month into their Nest pension, the 1.8% charge3 means they are immediately losing £3.60 each time they contribute.

Over a year, this adds up to £43.20, and over a decade, it’s £432 – and that’s before you even consider the compound growth that could be lost on that money.

NOW pension and Smart both charge users £1.75 per month as a ‘member administration charge’ on top of the AMC. For low earners struggling to save into their pension, this could prove a significant hit. For someone saving £300 into their pension annually, 7% of their savings is going to pay these monthly fees.

Comparing Fees

Fees are just one aspect of myriad considerations when figuring out the merits of a new provider. With a future savings crisis looming it’s crucial to make it both easy and attractive for employees to engage with their pension. Both the choice and performance of funds are important, and the quality of customer service is key. If you’re in the market for a new workplace pension, we’ve put together a list of the things you should consider in our How to choose a workplace pension provider article.

The extra charges make it challenging for employers to compare the costs of pensions. At Penfold, we aim to simplify this task by providing a transparent fee structure, making it easier to compare and contrast with other providers in the market. To help with this, read our comparison of different workplace pension providers. And for more information about Penfold's one simple fee (the AMC) read our pension charges page.

Penfold's Simplicity and Transparency

Experience Penfold's simplicity and transparency first-hand by scheduling a personalised demo. Our platform is designed to streamline pension management, making it a breeze for both accountants and their clients. Features like easy integration with existing accounting systems and a user-friendly interface underscore our commitment to simplifying pension management.

See how Penfold can transform pension management for your clients.

1. https://www.gov.uk/government/statistics/business-population-estimates-2022/business-population-estimates-for-the-uk-and-regions-2022-statistical-release-html

2. https://www.nowpensions.com/payroll-bureaux/costs-and-charges/

3. https://www.nestpensions.org.uk/schemeweb/nest/my-nest-pension/contributions-and-fees.html

Murray Humphrey

Penfold