2024/25 Tax Year Changes and What They Mean for You

Navigating Financial Changes in an Election Year

It’s election year and so hardly surprising that there are a slew of new and important changes being introduced as we enter a new financial year.

On April 6th each year new rules that impact our finances are unveiled and as the Conservative Party battles to try and keep hold of power it is no wonder that a raft of changes are on their way this time around in a bid to win over voters.

The main changes include cuts to National Insurance contributions, the abolition of the lifetime allowance, and an increase in the state pension. Below we look in more detail at those three adjustments and what the new rules will mean for you from the 2024/25 tax year onwards.

National Insurance Cuts: A Closer Look

Following a reduction from 12% to 10% earlier in January, Chancellor Jeremy Hunt announced a further cut in National Insurance contributions by two percentage points:

- For employees, rates will drop to 8%.

- For self-employed workers, rates are set at 6%.

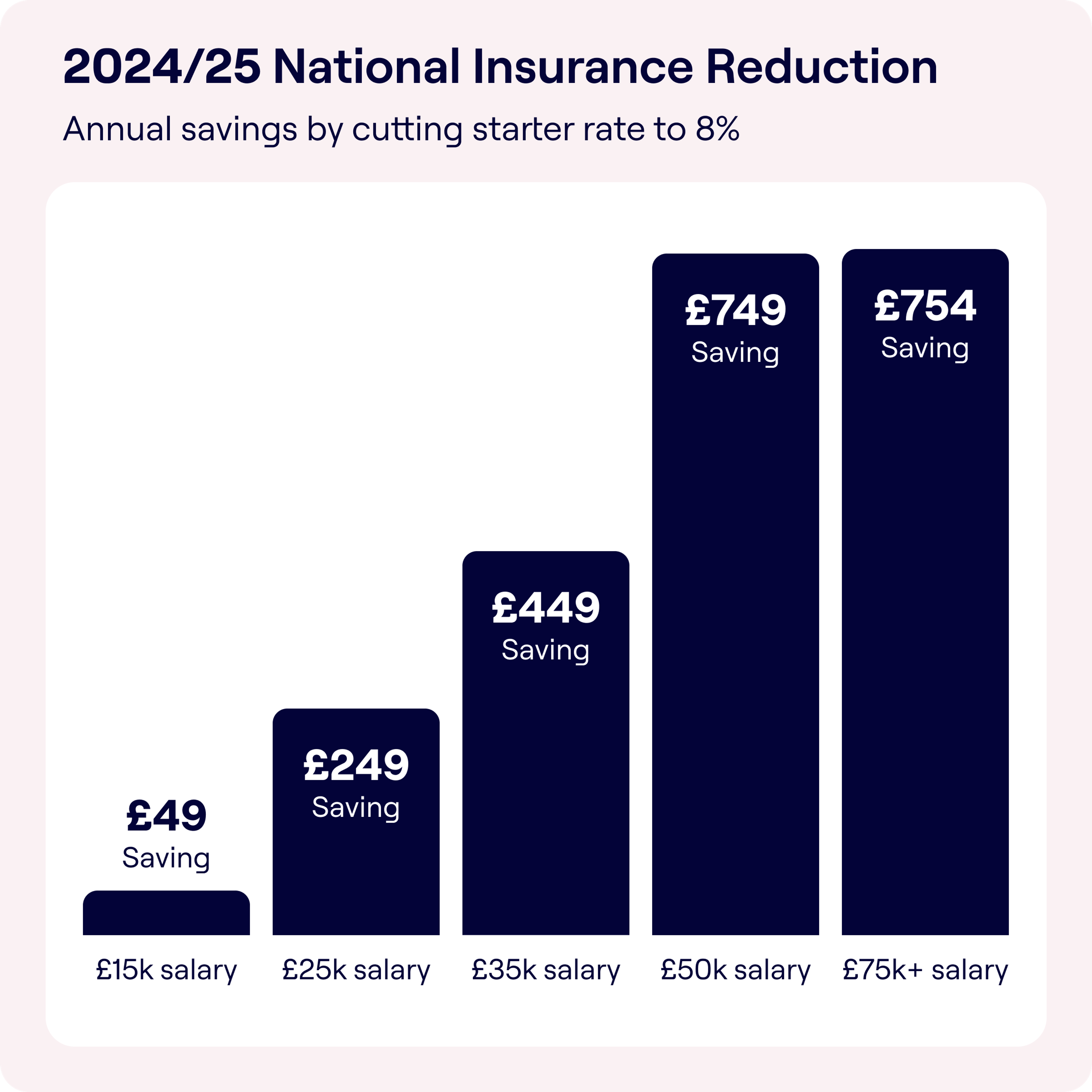

This tax on earned income previously saw employees paying 10% on earnings between £12,570 and £50,270, but from April 6th 2024 they will pay 8%, while the self-employed will pay 6%. There is no change to the 2% national insurance rate on earnings over £50,270.

While this might seem like a generous gift from the Chancellor, the fact that income tax thresholds have been frozen at their current levels – i.e. they haven’t increased in line with price rises and wages increases – means many taxpayers will not see much of a bump in their take-home pay.

Indeed, the Institute of Fiscal Studies states the National Insurance tax cut will not be enough to stop tax receipts for the government rising to record levels in 2028/9.

Looking at the National Insurance cut in isolation, however, the latest reduction amounts to an extra £248.60 a year for someone earning £25,000 and an almost £450-a-year boost for someone on £35,000. Those on £50,000 will get an extra £748.60. Around 29 million workers will benefit from the change.

Mandatory ‘class 2’ contributions – currently £3.45 a week – will also be ditched from April 6. However, those earning less than £6,725 a year can still opt to pay class 2 NICs to secure certain benefits, such as the state pension.

Lifetime Allowance Abolition

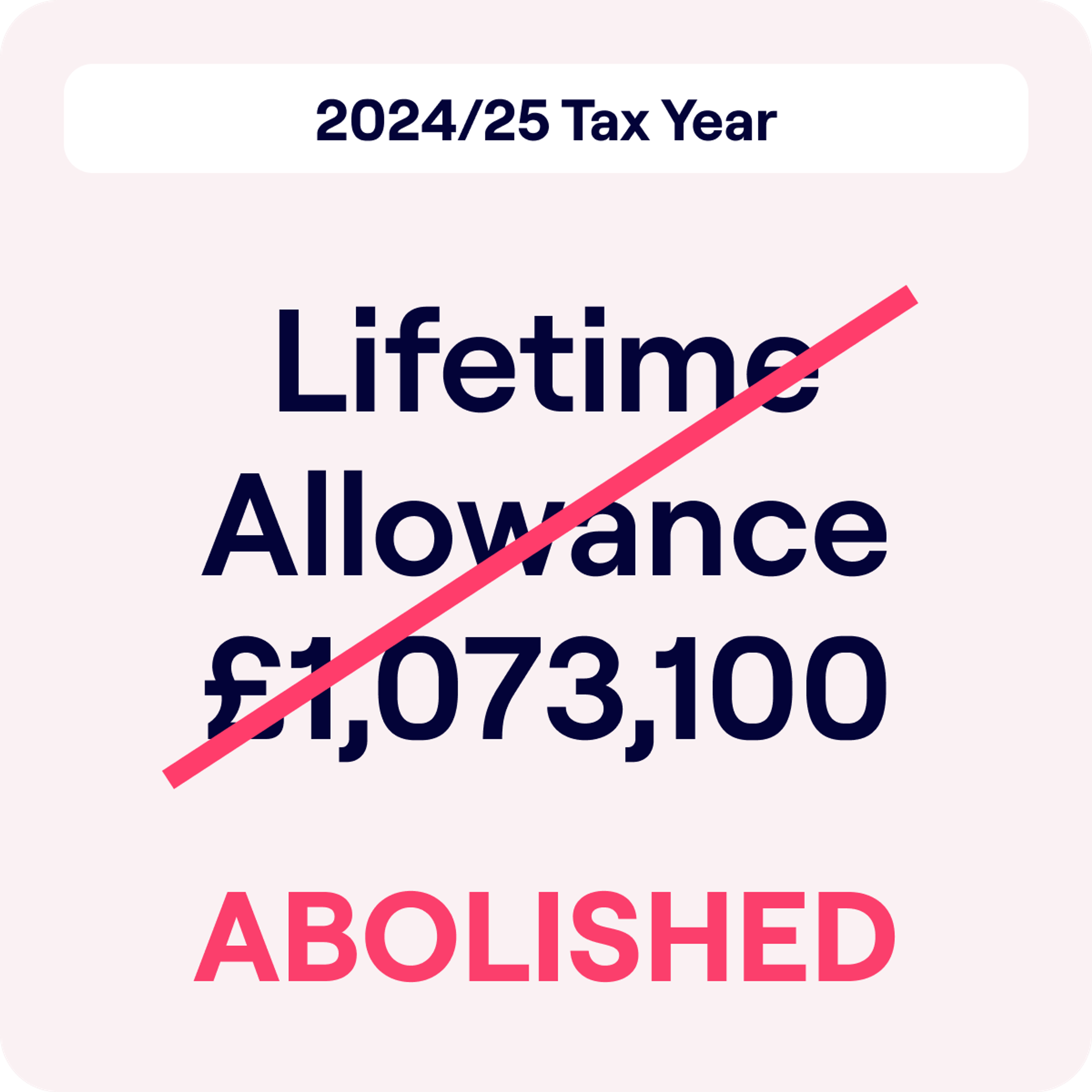

Firstly, what was the lifetime allowance? Well, it was the maximum amount you could draw from your pension without paying extra tax, which included a component of being able to receive up to 25% tax free. The lifetime allowance stood at £1,073,100, but the charge for breaching this was removed last year, with the allowance to be abolished altogether from the 2024/25 tax year.

Its abolishment was a surprise to many and was criticised as being a policy that only benefited the very rich. Its removal, however, does not mean we won’t have any rules in place as two new allowances are coming in: the lump sum allowance and the lump sum and death benefit allowance.

From April 6th 2024, an individual’s lump sum allowance will now be £268,275 (25% of the previous lifetime allowance). This is the amount that can be taken out of a pension tax free.

If an individual dies before 75, the lump sum and death benefit allowance up to £1,073,100 can be paid tax free to their beneficiaries, equivalent to the old lifetime allowance.

There are no changes to how death benefits are taxed where a death occurs after the age of 75. In this instance beneficiaries will be taxed at their marginal rates of income tax whether or not benefits are captured as a lump sum, inherited drawdown, or used to purchase an annuity.

One more allowance is also being introduced: the overseas transfer allowance, which covers transfers to qualifying recognised overseas pension schemes. This is also set at the level of the old lifetime allowance – £1,073,100.

State Pension Increase: Maintaining the Triple Lock

The amount you’ll get from the state pension will rise on April 6th 2024. The reason for this is because the government has pledged to keep hold of the ‘triple lock’, which each year guarantees that the state pension will rise by the highest of one of three measures: average earnings; inflation, as measured by the consumer prices index; or 2.5%.

As a result of keeping the triple-lock, which is widely viewed as an attempt by the government to secure the older vote, the state pension will rise by 8.5%. The triple lock was ushered in by the Conservative-Liberal Democrat coalition government in 2010 but was suspended for one year during the Covid epidemic as the figures for average earnings became distorted.

The latest increase means that those qualifying for a full new state pension will now get £221.20 a week (up from £203.85), while those who reached state pension age before April 2016, and who receive the older basic State Pension, will now get £169.50. This is up from £156.20. More than 12 million people currently get the state pension.

The state pension age rose to 66 by 2020 and is due to increase to 67 between 2026 and 2028.

Summary: A Mixed Bag of Financial Changes

Depending on who you are, the national insurance cuts, the state pension increase and the abolition of the lifetime allowance will come as welcome news. But, while the government has given with one hand, the fact that income tax thresholds have been frozen at their current levels means the chancellor will be taking away with the other.

With the election looming, these financial adjustments will no doubt play a crucial role in shaping voter sentiment and the broader economic landscape. By understanding these shifts, voters can make informed decisions, considering not just the immediate benefits but the long-term impacts on their financial well-being.